06 Mar Mortgage Rate Scandal

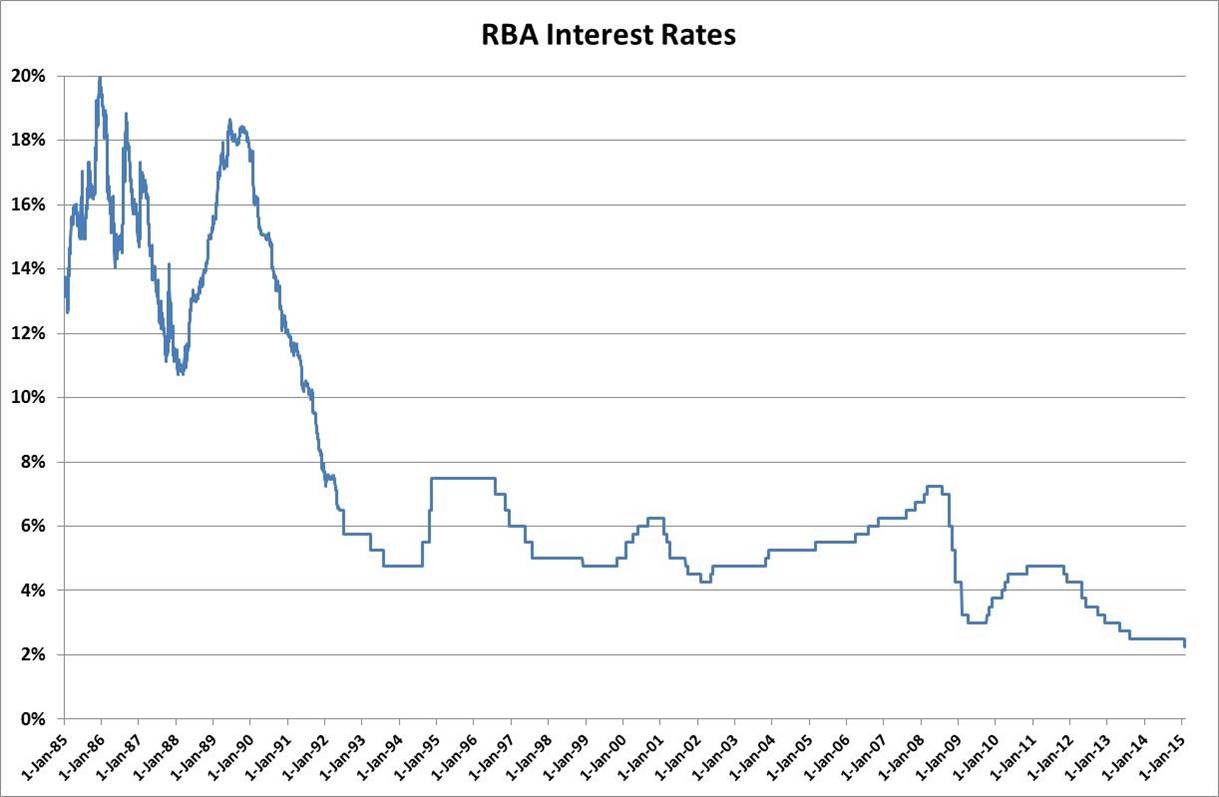

There is no question that the high mortgage interest rates of the late 1980s limited housing affordability. Because of this, I and many others, lost our first homes and financially struggled for a long period before saving enough money to buy another one. It is what I learnt from this experience that I shall pass on to you now.

Nowadays, just about everyone who buys a house has a mortgage. When a client goes directly to a bank, the way the loan is sold to them is usually based on interest rates rather than knowing how the loan actually works. Quite often a discussion about ways in which the debt can be paid down faster has not even taken place.

Mortgage rates are frequently advertised in the media, social media and the banks themselves. In the 80’s this did not happen and people never refinanced because of interest rates. They stayed with their loan and paid it off.

There is a lot of speculation about which direction the rates will move and this obsession with interest rates has become the focal point of the financial decision-making process. Don’t be fooled! Although it’s tempting to focus on interest rates as a starting point for comparing your mortgage options, understanding your loan structure is far more important.

What the banks don’t tell us and do not want us to know, is that the interest rate itself, plays only a small part in how much interest you pay, and how fast you will pay back your loan. The real secret to paying the loan off quicker, has almost everything to do with how the loan has been set up. (Structured). Generally, traditional home loans are structured over a 30-year term. This allows the lenders (primarily banks) to maximise interest whilst making the repayments look minimal. This entices you into the loan agreement.

Have you noticed that loans are getting bigger and rates are getting cheaper? The longer the term, the lower the repayments. As house prices increase, loan terms will become longer (50 years plus) to enable affordability. There are already loans of 75 years and more in Japan and Europe. Australian bank profits have increased 4 times more today at emergency low rates of 1.5% than what they were in the 80’s at their peak when rates went as high as 20%. The average loan in the 80’s was $100k – today it’s $800k … the figures below are staggering! What will bank profits be if the loan goes to 60-70 years. Banks want this to happen so they can push out more debt and make more profit.

The key principle of mortgage reduction is that “interest is calculated on the daily balance”. So how do we beat it?

The day-to-day balance of the mortgage account has a significant impact on the interest charged to your home loan, and therefore the term of your loan. So, by utilising all of your money to your advantage we can prove that a loan with a higher interest rate but better structure, can easily outperform a loan with a lower interest rate and poor structure.

The truth is, no one has ever paid their house off any faster just because they got a cheaper rate! The only way you can pay your house off faster is to reduce time and the only way you can do that is to put more money into your mortgage.

You will get a lot of benefit out of talking to a Pivotal Financial Broker, we can help you to structure your loan properly rather than just walking into a bank.

No Comments